Shepherd Outsourcing opened its doors in 2021, and has been providing great services to the ARM industry ever since.

About

Address

©2024 by Shepherd Outsourcing.

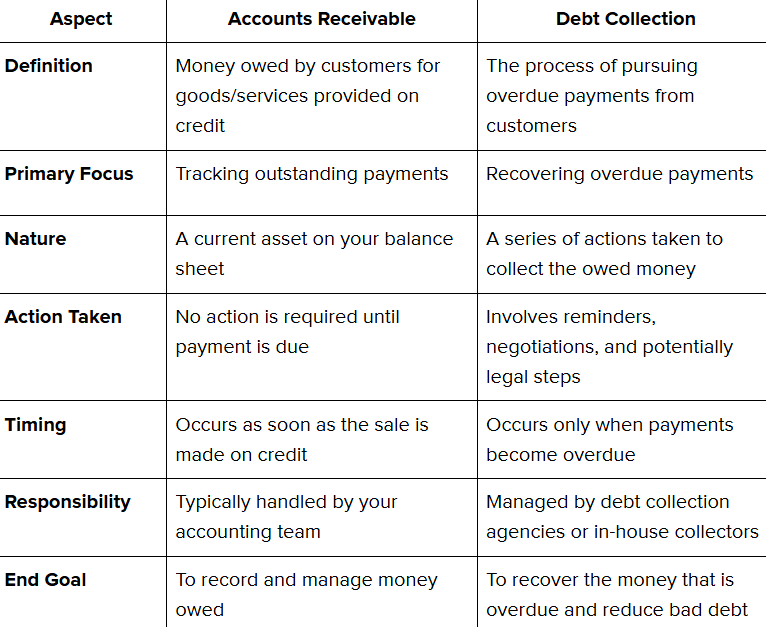

Understanding the difference between accounts receivable and debt collection is key when managing finances. While both are related to the money your business is owed, they play very different roles in your cash flow process. Accounts receivable refers to the money you're waiting to receive from customers, while debt collection involves the steps you take when those payments are overdue. Understanding these concepts will help you streamline your financial operations and stay on top of what’s owed to you.

Let’s dive deeper into what each of these terms means.

Accounts Receivable (AR) is the money your customers owe you for goods or services you’ve provided but haven't been paid for yet. Think of it as a kind of IOU from your customers. When you make a sale on credit, it goes into your AR. This balance is part of your business's current assets because, ideally, you expect to collect that money soon.

On the other hand, AR Debt Collection is the process you follow when those accounts receivable turn into overdue payments. It’s the steps to remind, follow up, and sometimes even escalate matters to recover the unpaid money. This could involve sending reminder notices, contacting collection agencies, or taking legal action if necessary. While accounts receivable is more about tracking the money owed, AR debt collection is about ensuring that money gets to you.

In short, AR is about what’s due, while AR debt collection is about making it happen.

Managing your accounts receivable (AR) effectively is crucial for maintaining a healthy cash flow in your business. Here are the key components to ensure your AR process runs smoothly and efficiently:

Setting clear credit terms helps prevent confusion and ensures customers understand when and how payments are due. Having defined policies regarding who qualifies for credit, credit limits, and payment terms is essential for minimizing the risk of overdue payments.

Sending accurate and timely invoices is critical. Ensure invoices reflect the agreed-upon terms, including the correct amounts, due dates, and applicable discounts or penalties. Delays or mistakes in invoicing can confuse and delay payment.

Monitoring your accounts receivable regularly helps identify overdue accounts early. Use aging reports to track outstanding invoices and spot patterns of late payments. The sooner you identify an issue, the easier it is to take corrective action.

Open communication is vital for resolving payment issues. If a customer cannot pay on time, discuss potential solutions, such as payment plans or adjusted terms, rather than letting the situation escalate. Maintaining positive relationships helps secure future payments.

Setting up a clear process for following up on overdue invoices is crucial. This could include sending reminder emails, making phone calls, or even sending final notices. The more proactive you are, the higher the chances of recovering outstanding balances before they become problematic.

By focusing on these components, you can create a robust system for managing your accounts receivable, reduce the risk of overdue accounts, and improve your business's overall cash flow.

An effective debt collection process is essential for recovering overdue payments and maintaining a healthy cash flow. By implementing a structured approach, you can improve your chances of recovering what’s owed to your business while maintaining good customer relationships. Here are the key components of a successful debt collection process:

Clear and consistent policies are the foundation of an effective debt collection process. These should outline your steps for collecting debts when to escalate issues, and how you’ll handle disputes. A defined policy ensures transparency and helps avoid confusion when dealing with late payments.

The first step in the collection process is sending a reminder once a payment is overdue. Typically, this involves a polite reminder via email or letter, often including a copy of the original invoice. The goal is to remind your customer of the outstanding balance and encourage payment without escalating the situation.

Follow-up communication is necessary if the payment is not made after the initial reminder. This could involve more formal letters, phone calls, or emails. Ensure your messages remain professional but firm, reiterating the importance of clearing the debt.

Sometimes, customers may be unable to pay the full amount immediately. In such cases, offering a payment plan can help facilitate recovery. Negotiate realistic terms for both parties, ensuring the payment plan is clear and enforceable. This step shows flexibility while still pursuing the payment.

If previous attempts to collect the debt have failed, it’s time to escalate the issue. Depending on your collection policies, this may involve senior management or legal advisors. The escalation process could also include final notices that warn customers of potential legal or financial consequences.

Many businesses turn to professional collection agencies if in-house collection efforts are unsuccessful. These agencies specialize in recovering outstanding debts and have the tools and expertise to handle tough cases. While they charge a fee or commission, they increase the chances of recovering the debt.

As a last resort, legal action may be necessary to recover the debt. This could involve filing a lawsuit against the debtor or seeking a court order for payment. Legal action can be expensive and time-consuming, but it may be your only option when all other attempts to collect the debt have failed.

By focusing on these components, you can implement a debt collection process that improves your chances of recovering outstanding payments, reduces the time it takes to collect, and helps maintain positive customer relationships.

While both accounts receivable and debt collection are related to the money your business is owed, they have distinct functions. Understanding these differences can help you manage your finances more effectively. Here’s a quick breakdown:

Let’s say you run a small business that sells office furniture. A customer orders a set of desks and chairs worth $5,000. However, instead of paying upfront, they ask for 30 days to settle the bill. You agree to deliver the furniture, leaving an outstanding invoice for $5,000 due in 30 days.

In this case, the $5,000 the customer owes you is accounts receivable. It’s an amount you expect to receive soon and is listed as an asset on your balance sheet. You’ll track this amount as part of your accounts receivable until the customer makes the payment.

Accounts receivable becomes a debt collection when the customer fails to pay within the agreed-upon terms, and the payment becomes overdue. Here's how the process generally unfolds:

To summarize, accounts receivable turn into debt collection when the money owed is overdue and the necessary follow-up steps, including external agencies or legal actions, are initiated to recover the funds.

A professional debt settlement service can offer crucial assistance when a debtor faces overwhelming debt. Shepherd Outsourcing Collections specializes in negotiating with creditors to reduce the total amount owed.

Here’s how our services can benefit you:

Managing accounts receivable and debt collection can be complex and time-consuming, especially when dealing with overdue payments or a large volume of customers. Businesses often face various challenges in ensuring their AR processes run smoothly and that debt collection efforts are effective. Let’s dive into the top five challenges that businesses face in this area:

Challenge: A growing issue in today’s business world is delayed payments. In fact, 81% of businesses report an increase in delayed payments, with 55% of B2B invoiced sales being overdue. This growing trend puts significant pressure on businesses and disrupts cash flow, making managing day-to-day operations like payroll, purchasing, and investments difficult.

Impact: Late payments can cause cash flow issues, leaving businesses struggling to cover expenses or meet financial obligations. If not addressed promptly, it could also lead to a build-up of bad debts and strained client relationships.

Solution: Regularly monitoring aging reports, sending timely reminders, and offering incentives for early payments can encourage customers to pay on time. However, many businesses turn to professional debt collection services like Shepherd Outsourcing Collections as delayed payments become more common.

Shepherd Outsourcing helps B2B and B2C creditors recover overdue payments by negotiating directly with debtors, ensuring better cash flow, and reducing bad debt risks.

Challenge: Disputes between businesses and customers regarding invoices or payment terms are another significant challenge. This could involve billing, pricing, or goods/services discrepancies.

Impact: Disputes delay payment, requiring additional time and effort to resolve. Inaccurate billing or misunderstandings can damage customer relationships and cause frustration.

Solution: Ensure invoicing is accurate, clear, and sent promptly. Keeping open communication with customers and addressing concerns quickly can prevent disputes from escalating. Regular audits and checks can help reduce errors in billing.

Challenge: An inefficient or inconsistent follow-up process can lead to overdue accounts slipping through the cracks. If reminders aren’t sent promptly or if they aren’t firm enough, customers may delay payments without consequence.

Impact: Failure to follow up effectively can result in many overdue invoices, affecting cash flow and increasing the risk of bad debts.

Solution: Automating the follow-up process can help ensure that reminders are sent on time. Having a clear follow-up schedule and using multiple communication methods (emails, phone calls, or letters) can increase the chances of collecting payments on time.

Challenge: Extending credit to customers who may not be financially stable or have poor credit histories increases the risk of bad debt. Assessing a customer’s ability to pay can be difficult, especially with new customers or in uncertain economic times.

Impact: High bad debt levels can significantly affect profitability and lead to financial instability, making investing in growth or managing daily operations hard.

Solution: Implement credit checks and set limits based on customer history. Offering different payment terms or requiring partial payments upfront for high-risk customers can reduce the risk of bad debt.

Technology can enhance accuracy, reduce human error, and improve efficiency, leading to faster payments and better cash flow management. Let’s explore how technology can help businesses manage AR and debt collection more effectively and why it’s becoming increasingly crucial in the industry.

A study by Cognitive Market Research states that the global debt collection services market, which is expected to reach approximately $30.52 billion by 2025, is seeing significant growth driven by technological advancements like automated billing systems.

As of 2023, AI adoption in debt collection was still in its early stages, with only 11% of companies using it, but many are planning to integrate it shortly.

Understanding the differences between accounts receivable and debt collection is crucial for maintaining healthy cash flow and reducing financial risks. While accounts receivable focuses on tracking what’s owed, debt collection involves actively recovering overdue payments. Businesses can ensure smooth operations and protect their bottom line by effectively managing both processes.

If you’re struggling with overdue accounts or need help negotiating settlements, Shepherd Outsourcing Collections can support you. We specialize in reducing debt through expert negotiations, offering tailored solutions, and ensuring legal compliance. Reach out today for professional help managing your receivables and improving your financial outcomes.

1. What is the main difference between accounts receivable and debt collection?

A: Accounts receivable refers to the amounts owed to your business by customers for goods or services provided on credit, while debt collection is the process of actively recovering overdue payments. Essentially, accounts receivable is about tracking outstanding payments, and debt collection is about ensuring those payments are received.

2. Why must businesses manage accounts receivable and debt collection?

A: Proper management of both accounts receivable and debt collection is critical for maintaining healthy cash flow. While accounts receivable tracks the money owed, debt collection ensures that overdue payments are recovered. Without effective management, businesses risk facing financial strain and bad debt.

3. When should businesses start debt collection efforts?

A: Debt collection efforts should start once a payment is overdue. Following up promptly with reminder emails, phone calls, or letters is important. If the payment remains unpaid after multiple attempts, businesses may consider escalating the issue to a collection agency or taking legal action.

4. How can technology help with accounts receivable and debt collection?

A: Technology can significantly streamline accounts receivable and debt collection by automating invoicing, payment reminders, and follow-ups. Additionally, AI tools and debt collection software can help businesses predict payment behaviors, prioritize overdue accounts, and improve efficiency in recovering debts.

5. Why should businesses consider using debt collection agencies?

A: When internal efforts fail, debt collection agencies like Shepherd Outsourcing Collections can help recover overdue payments. Agencies specialize in negotiating with debtors, ensuring legal compliance, and offering tailored solutions, making the process less stressful for businesses and increasing the likelihood of recovering funds.

©2024 by Shepherd Outsourcing.